World Economic Situation And Prospects: November 2021 Briefing, No. 155

Advanced economies are facing large-scale labour shortages

Advanced economies are facing large-scale labour shortages

The outbreak of the COVID-19 pandemic since the beginning of 2020 caused an unprecedented and severely disruptive shock to labour markets worldwide. Despite the immense efforts to protect employment and to support businesses undertaken in the majority of countries around the globe, unemployment reached alarming levels in 2020, leading to erosion of incomes and pushing many households into poverty. Although the global economy has been gradually rebounding over the course of 2021, the speed of job creation is generally lagging to compensate for the earlier employment losses, especially in developing economies. This is especially true for those sectors that were hit particularly hard by the pandemic, such as tourism, travel, leisure and the hospitality industry. Many geographic regions, such as Latin America and the Caribbean, are facing the prospect of an economic recovery that is accompanied by protracted high rates of unemployment and precarious increases in informality. According to the ILO, around 220 million people are expected to remain unemployed globally in 2021, while the global unemployment rate may reach 6.3 per cent, falling to only 5.7 in 2022, which still would be above the pre-pandemic level of 5.4 per cent registered in 2019.

At the same time, against the background of the global labour market distress, many developed economies, including Australia, Canada, the United States, and numerous economies in Europe, are confronted with acute labour shortages in specific sectors, threatening to obstruct the global recovery, although some of those countries still have unemployment rates above the pre- pandemic level.

The manufacturing sector worldwide is one of those that are currently experiencing a shortage of workers. Manufacturing output in Europe, in particular, has already fully recovered from the crisis in the first half of 2021, rebounding along with international trade. Producers are trying to address the huge backlogs of earlier orders caused by lockdowns and suspensions of production activity. Many services in Europe are also gradually returning to full-time activity. And while some of European workers still remain furloughed and are waiting to return to work (labour retentions schemes in the OECD area reached 20 per cent of the total employment during the peak of the crisis), multiple businesses are struggling to fill open vacancies (see figure 1 for Europe’s vacancy rates).

In some European countries, in particular, in the Czech Republic and Germany, the unemployment rate in August 2021 subsided to low single-digit levels, at around or below 3 per cent; meanwhile the vacancy rate in the Czech Republic has reached 5 per cent. In September 2021, over 27 per cent of businesses operating in the construction sector in Europe referred to the shortage of workers as the main factor limiting economic activity. Meanwhile, the shortage of truck drivers in Europe (but also in the US and Canada), leading to the disruption and reconfiguration of the local and regional supply chains (as ships are diverted from one port to another delaying supplies arrivals) has become one of the most immediate issues to resolve. The number of open positions in the trucking industry virtually doubled in the UK since the beginning of the year. Some estimates put the truck driver shortage at 100,000 for the UK alone and at 400,000 for Europe as a whole. In the US, where the economy rebounded strongly in the second quarter of 2021, the number of total job openings exceeded 11 million in July and stood at over 10.4 million in August, with the vacancy rate reaching 6.6 per cent, while the number of unemployed workers edged down to 8.4 million. Severe labour shortages are also registered in Australia and Canada. Moreover, difficulty in finding workers is not just a developed economy problem – in the Russian Federation, the need for construction workers, in particular, forced the government in October 2021 to abolish entry bans imposed earlier on 300,000 workers from Tajikistan and Uzbekistan.

In some European countries, in particular, in the Czech Republic and Germany, the unemployment rate in August 2021 subsided to low single-digit levels, at around or below 3 per cent; meanwhile the vacancy rate in the Czech Republic has reached 5 per cent. In September 2021, over 27 per cent of businesses operating in the construction sector in Europe referred to the shortage of workers as the main factor limiting economic activity. Meanwhile, the shortage of truck drivers in Europe (but also in the US and Canada), leading to the disruption and reconfiguration of the local and regional supply chains (as ships are diverted from one port to another delaying supplies arrivals) has become one of the most immediate issues to resolve. The number of open positions in the trucking industry virtually doubled in the UK since the beginning of the year. Some estimates put the truck driver shortage at 100,000 for the UK alone and at 400,000 for Europe as a whole. In the US, where the economy rebounded strongly in the second quarter of 2021, the number of total job openings exceeded 11 million in July and stood at over 10.4 million in August, with the vacancy rate reaching 6.6 per cent, while the number of unemployed workers edged down to 8.4 million. Severe labour shortages are also registered in Australia and Canada. Moreover, difficulty in finding workers is not just a developed economy problem – in the Russian Federation, the need for construction workers, in particular, forced the government in October 2021 to abolish entry bans imposed earlier on 300,000 workers from Tajikistan and Uzbekistan.

This seemingly paradoxical situation of persistent high unemployment accompanied with serious labour shortages is explained by a confluence of various factors. An unbalanced rebound of the global economy across different sectors and changes in the composition of aggregate demand are among the reasons causing shifts in the labour demand pattern. Even more importantly, the pandemic has also changed the pattern of labour supply, creating difficulty for employers to find qualified candidates; among other factors, the risks posed by COVID-19 made many occupations much less attractive for workers, leading to increases in reservation wages. The resulting labour shortages are not only holding back recovery from the crisis induced by the COVID-19 pandemic, but also are damaging the longer-run trajectory of the potential output growth for many countries.

There are many common factors across the economies explaining the current difficulties for businesses to find employees; but there are also individual country peculiarities. While in Europe, especially in the EU member states from Eastern Europe, the massive deficit of labour has already been observed for a long period of time prior to the COVID-19 pandemic, in the United States and Canada labour shortfalls at such scale appears to be a relatively recent phenomenon.

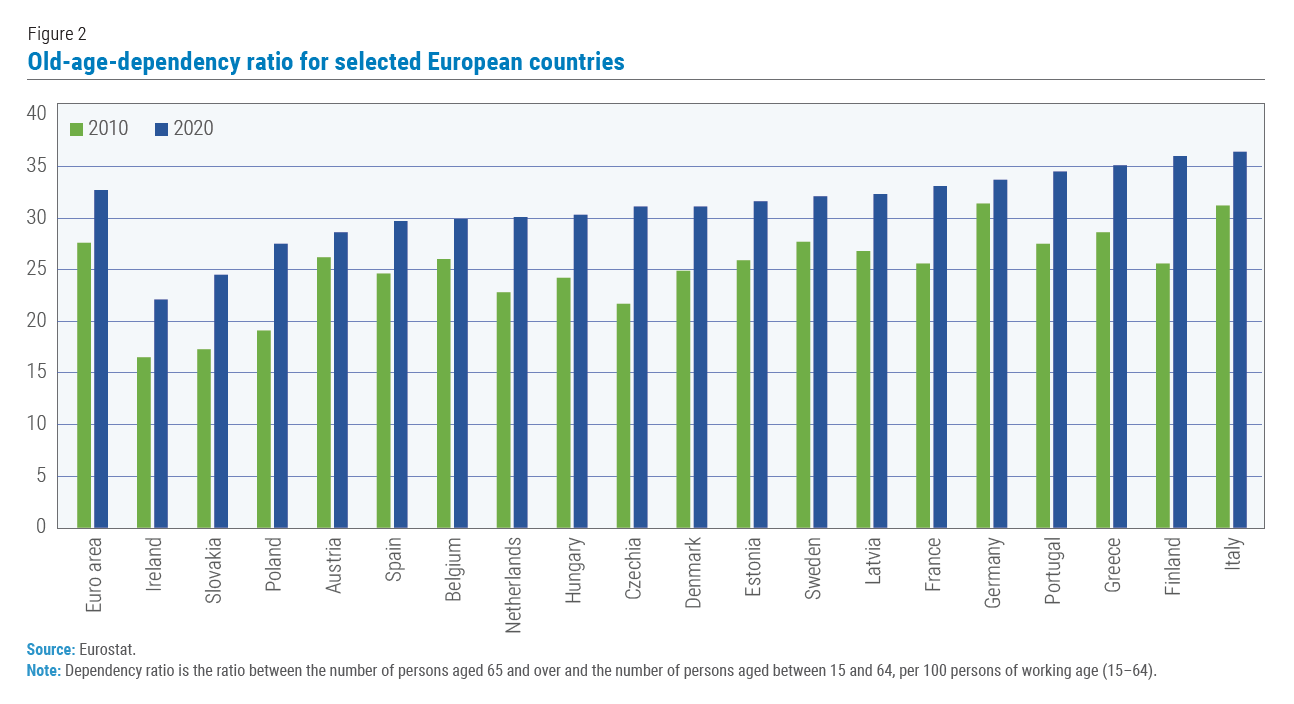

For the European countries, one of reasons for the persistent worker shortages is the ageing population (figure 2), which also implies an increase in the number of retirements in the medium-term, not likely to be offset by young people joining the labour force. For some of those EU members that joined the Union in 2004, 2007 and 2013, the demographic factor is aggravated by the massive outward migration, as workers, especially those of the younger generation, took advantage of the EU’s common labour market and moved to more prosperous European countries (even though not all of the EU members states immediately extended labour mobility to the new entrants). Some estimates put the loss of Lithuania’s workforce, for example, as high as 30 per cent since May 2004. In addition, Europe for many years has been facing structural mismatches between labour supply and demand, even in case of efficient education systems tailored to a particular labour market. The current shortage of workers in Germany is estimated at 400,000 people, and most of those open positions require highly skilled workers. To a certain extent, Western European countries were able to address those shortages by absorbing migrant workers from Eastern Europe. The COVID-19 pandemic, however, has disrupted migration patterns, and certain travel restrictions still remain in place, while many of the migrant workers returned home. Brexit also caused additional complications for hiring migrant labour in the United Kingdom.

On top of the existing problems, many workers in the OECD countries have left their workplace in 2021, looking for better conditions, including flexible working hours and ability to work remotely. In the US, the number of people leaving their jobs surged in August, reaching 2.9 per cent of the workforce (in 2020, monthly quit rate ranged from 1.9 to 2.4 per cent), among them almost 1,212,000 workers in the leisure and hospitality (mostly in accommodation and food) industries. The pandemic has also triggered a wave of early retirements in the US and Canada in particular, especially among the frontline workers. The labour force participation rate in the US that has already been declining since early 2000s, plunged during the pandemic in the second quarter of 2020, and has recovered only partially since then, stabilizing at a level around 61 per cent in the second and third quarters of 2021. Although the number of COVID-19 infections subsided somewhat in early 2021 along with the progress in vaccination rates, the recent surge in cases during the summer months, including the spread of the delta variant, has deterred some potential workers from returning to the labour market. As schools and childcare centres remained closed, some of the prospective workers had to deal with domestic care responsibilities. Some others decided to relocate to other industries and look for more safe and permanent positions.

In some cases, the current shortfall in labour in the advanced economies is explained by the “moral hazard effect” of the massive fiscal response to the pandemic undertaken in 2020–2021. In the United States, in particular, the fiscal stimulus included relief bills providing recipients of state unemployment an additional $600 in weekly benefits (eventually reduced to $300); benefits were paid at federal and state level to those workers who are usually not eligible to receive them (for example workers in the so-called “gig economy” and workers hired by contractors), along with mailing stimulus checks to the households. It was anticipated that suspension of those payments, most of which have already expired in September 2021, would encourage a massive return to the jobs market. However, the experience of those US States where the additionally introduced benefits have already expired over the summer, did not confirm the expectations of a massive return to work. Some studies found extremely weak disincentive effect from the payments of extra benefits. In fact, the pandemic highlighted more structural problems in labour markets, including low wages, dissatisfaction with work, and poor working conditions, implying that the reasons discouraging people from work are much deeper and will require larger efforts to resolve.

Looking ahead, the shortage of workers faced by numerous industries around the world may lead to different economic scenarios, in case the problem becomes long-lasting and persists after the expiration of additional benefits payments and even after the eventual containment of the pandemic. On the one hand, it may lead to increased productivity, stimulating investment in innovation, research and development and more capital-intensive technologies. There are some indications that gains in labour productivity are already taking place in the OECD area, however, it is still premature to make any assessments on the basis of few quarterly observations, as short-term swings in productivity do not ensure shaping of a sustainable long-term trend, especially when workers mainly from labour-intensive sectors temporarily quit economic activity.

On the other hand, not all of the industries currently facing labour shortages are subject to rapid automation and there may be a significant time lag before worker replacement is put in place. For example, the current shortage of truck drivers, observed all across Europe and many other countries, is creating immediate problems and can hardly be resolved by automation in the near-term. The same may be true for the restaurant, health care, and hospitality industries. And while innovation and increased automation may help to address the labour bottlenecks in the medium term, in the longer run it may lead to a confluence of social and economic problems, creating persistent structural unemployment, contributing to income inequality and eroding social cohesion.

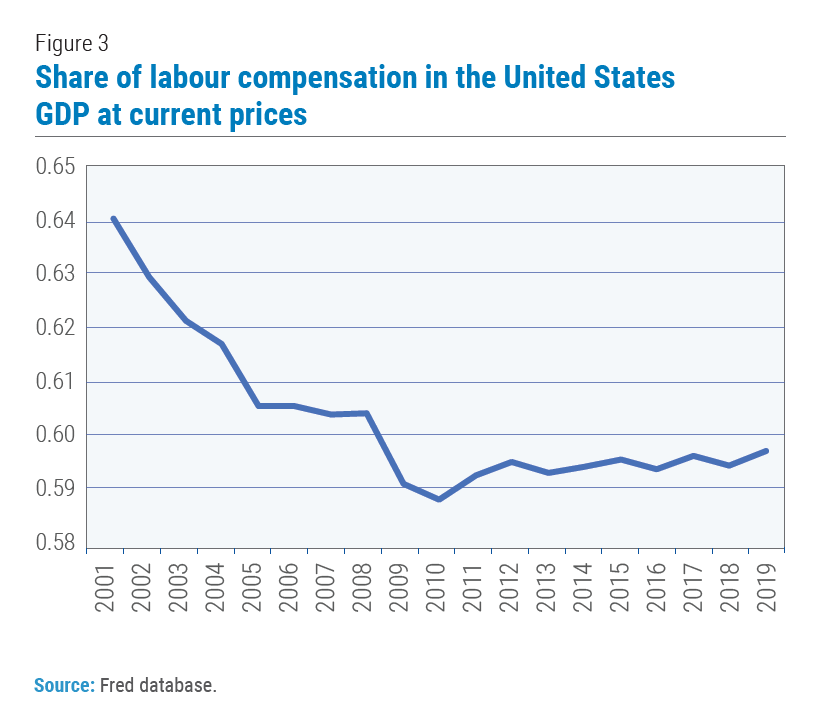

Concordantly, a more positive scenario would entail the development and implementation of a set of active policies to address the twin problem of elevated unemployment and acute labour shortages, both by governments and also by the private sector. One of the much-needed actions would be to increase wages, in particular, for the relatively lower-skilled jobs. Among the major economies, wages in the US have been stagnating in real terms for most of the population and their share in GDP persistently declined, while workers’ bargaining power has virtually evaporated (figure 3). This was mirrored by the increased share of corporate profits. These numbers should be treated with caution, since many small business owners and the self-employed even in the low-skill category report their earnings as corporate income, but they still indicate that the business sector, with the exception of small businesses perhaps, will be able to absorb lower profitability under increased labour costs. In addition, provision of affordable housing is imperative for increasing intra-economy labour mobility (which in the US, for example, has been persistently declining over the last two decades) and investment into safer workplaces (including expanding the availability of vaccines) and better working conditions, such as offering flexible work hours and an option to work remotely, are essential for stimulating workers to become economically active.

Concordantly, a more positive scenario would entail the development and implementation of a set of active policies to address the twin problem of elevated unemployment and acute labour shortages, both by governments and also by the private sector. One of the much-needed actions would be to increase wages, in particular, for the relatively lower-skilled jobs. Among the major economies, wages in the US have been stagnating in real terms for most of the population and their share in GDP persistently declined, while workers’ bargaining power has virtually evaporated (figure 3). This was mirrored by the increased share of corporate profits. These numbers should be treated with caution, since many small business owners and the self-employed even in the low-skill category report their earnings as corporate income, but they still indicate that the business sector, with the exception of small businesses perhaps, will be able to absorb lower profitability under increased labour costs. In addition, provision of affordable housing is imperative for increasing intra-economy labour mobility (which in the US, for example, has been persistently declining over the last two decades) and investment into safer workplaces (including expanding the availability of vaccines) and better working conditions, such as offering flexible work hours and an option to work remotely, are essential for stimulating workers to become economically active.

To mitigate the entrenched mismatches between labour supply and demand and increase economic activity of the population, active training will also be needed in order to improve workers’ skills and to adjust them to the current labour market situation. Not only should active labour market policies include profound analysis of labour market trends, training and placement, matchmaking between companies and jobseekers, provision of tax incentives for companies expanding their workforce, expansion of public employment services, but it should also be accessible for the vulnerable segments of the population.

Follow Us